Maximize gains with portfolio rebalancing in crypto

Maximize gains with portfolio rebalancing in crypto

Many crypto traders hesitate to rebalance their portfolios, fearing they’ll lock in losses or miss out on explosive gains from their winning coins. This misconception keeps investors stuck in risky, unbalanced positions that expose them to unnecessary volatility and drawdowns. Portfolio rebalancing actually improves long-term returns by enforcing disciplined risk management and capturing gains systematically. This article explains proven rebalancing methods, reveals data-backed performance benefits, and shows you how to optimize frequency while minimizing costs and taxes.

Key Takeaways

| Point | Details |

|---|---|

| Restores target allocations | Rebalancing trims winners and adds to losers to keep the portfolio aligned with your defined risk and avoid overexposure to a single asset. |

| Automation outperforms manual | Automated systems monitor markets across exchanges and execute trades to reduce complexity and maintain disciplined strategy. |

| Threshold based rebalancing | Drift triggers reduce unnecessary trades by acting only when allocations diverge beyond a set threshold. |

| Empirical performance gains | Data indicates rebalancing improves risk adjusted returns versus buy and hold in crypto. |

What is portfolio rebalancing and why it matters in crypto

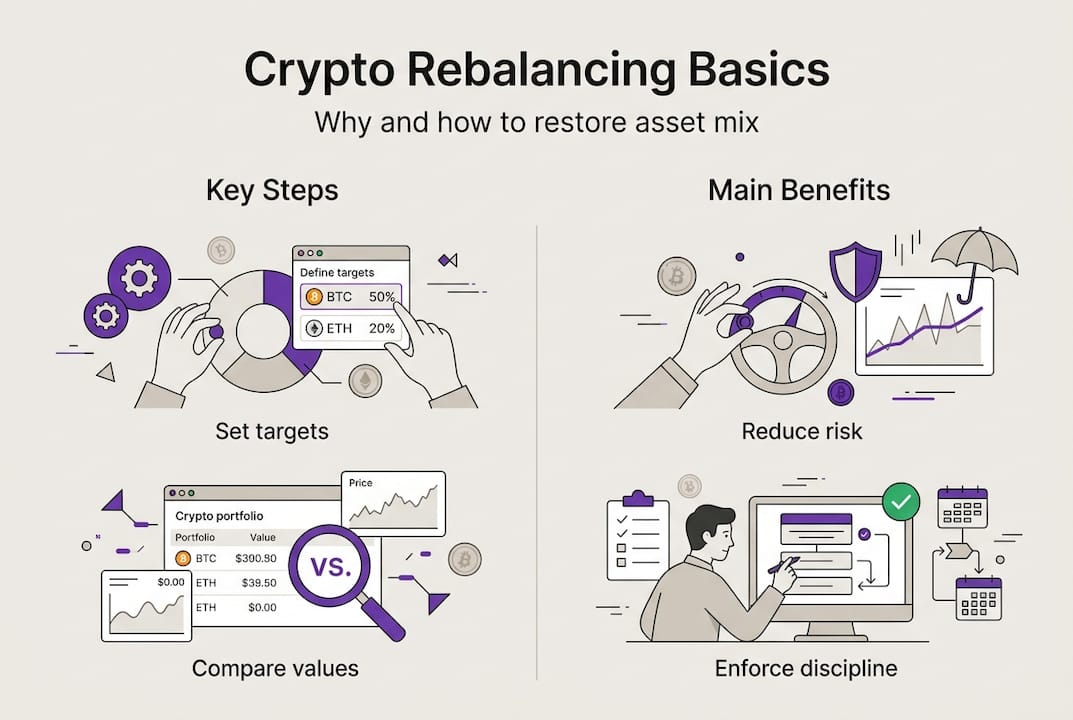

Portfolio rebalancing in crypto restores target asset allocations, managing risk by preventing over-concentration in volatile winners. When you set up a portfolio, you define target percentages for each asset based on your risk tolerance and investment goals. Bitcoin might represent 40%, Ethereum 30%, and altcoins 30% of your holdings. Market movements inevitably push these allocations off target as some coins surge while others lag.

Cryptocurrency markets amplify this drift problem dramatically. A coin that doubles in price can suddenly represent 60% of your portfolio instead of 30%, exposing you to massive downside if that asset corrects. This concentration risk is exactly what crypto rebalancing addresses by systematically selling portions of outperformers and buying underperformers.

The beauty of rebalancing lies in its counterintuitive mechanics. By trimming winners and adding to losers, you’re literally buying low and selling high on autopilot. This disciplined approach removes emotion from trading decisions and enforces a systematic profit-taking strategy that most manual traders struggle to execute consistently.

“Rebalancing is the only free lunch in investing because it reduces risk while maintaining or improving returns through forced contrarian behavior.”

Why volatile crypto markets make rebalancing crucial:

- Price swings of 20-50% in days can destroy carefully planned allocations

- Concentration in a single winning coin creates catastrophic loss potential

- Emotional attachment to winners prevents rational profit-taking

- Systematic rebalancing removes psychological barriers to selling

The crypto rebalancing glossary defines this process as the periodic adjustment of portfolio weights to maintain desired risk exposure. Without rebalancing, your portfolio gradually becomes whatever the market decides, not what your strategy requires.

Common rebalancing strategies and how they work

Key methodologies include periodic, threshold-based, constant mix, risk parity, and automated AI-driven strategies. Each approach offers distinct advantages depending on your portfolio size, trading costs, and risk tolerance. Understanding these methods helps you choose the right framework for your investment goals.

Periodic rebalancing operates on fixed calendar intervals regardless of market movements. You might rebalance monthly, quarterly, or annually on predetermined dates. This method offers simplicity and predictability but ignores actual portfolio drift, potentially missing critical rebalancing opportunities or triggering unnecessary trades when allocations remain close to target.

Threshold-based rebalancing triggers only when allocations drift beyond specified percentages. If you set a 5% threshold and Bitcoin grows from 40% to 46% of your portfolio, you rebalance. This approach responds to actual need rather than arbitrary timing, reducing transaction costs while maintaining control.

Automated strategies excel by enabling dynamic, low-cost, volatility-responsive rebalancing, outperforming manual methods. AI-powered systems can monitor multiple portfolios across exchanges simultaneously, executing optimal trades based on real-time market conditions and gas fees.

| Strategy | How it works | Best for |

|---|---|---|

| Periodic | Rebalance every fixed interval (monthly, quarterly) | Simple portfolios, predictable tax planning |

| Threshold | Rebalance when drift exceeds 5-10% | Cost-conscious traders, volatile markets |

| Constant mix | Maintain fixed proportions by continuous adjustment | Active traders, liquid portfolios |

| Risk parity | Balance risk contribution across assets | Sophisticated investors, multi-asset portfolios |

| Automated AI | Dynamic adjustment based on market signals | All portfolio sizes, multiple exchanges |

Constant mix strategies maintain fixed proportions through continuous small adjustments. When prices move, you immediately buy the dip and sell the rip to restore balance. This aggressive approach works best in ranging markets but can generate excessive trading costs in strong trends.

Risk parity and volatility-weighted approaches focus on equalizing risk contributions rather than dollar allocations. A highly volatile altcoin might represent only 10% of portfolio value but contribute 40% of total risk. These sophisticated methods adjust position sizes based on realized volatility to achieve true diversification.

The five-step rebalancing process:

- Calculate current asset allocations as percentages of total portfolio value

- Compare current allocations against target weights

- Determine required buy and sell quantities to restore targets

- Execute trades in optimal order to minimize slippage and fees

- Document transactions for tax reporting and performance tracking

Automated portfolio balancing removes the manual calculation burden and execution complexity. Modern platforms connect to exchanges via API, monitor positions continuously, and execute rebalancing trades automatically based on your chosen strategy and thresholds.

Automated portfolio management systems can also optimize trade timing to capture favorable spreads and minimize market impact, especially important for larger portfolios where single trades can move prices.

Empirical benefits and real-world performance of rebalancing

Weekly rebalancing yielded Sharpe 1.2 with 26.7% return and 28% volatility; dynamic RL portfolios gained 85% cumulative versus 65% buy-and-hold. These performance improvements aren’t theoretical, they represent actual results from systematic rebalancing strategies applied to cryptocurrency portfolios over multi-year periods.

The Sharpe ratio measures risk-adjusted returns by dividing excess return by volatility. A Sharpe of 1.2 indicates you earned 1.2 units of return for each unit of risk taken. Buy-and-hold crypto portfolios typically achieve Sharpe ratios between 0.6 and 0.9, making the 1.2 figure a substantial improvement in capital efficiency.

Rebalancing enforces sell-high/buy-low behavior reducing portfolio drawdowns significantly. During the 2022 crypto winter, rebalanced portfolios experienced 35-40% maximum drawdowns compared to 55-65% for buy-and-hold positions. This downside protection matters enormously for portfolio survival and psychological endurance during bear markets.

| Metric | Buy-and-hold | Quarterly rebalance | Weekly rebalance |

|---|---|---|---|

| Cumulative return | 65% | 78% | 85% |

| Annualized volatility | 42% | 35% | 28% |

| Sharpe ratio | 0.71 | 0.95 | 1.20 |

| Maximum drawdown | 58% | 43% | 38% |

These numbers reveal why sophisticated crypto investors prioritize portfolio rebalancing as a core strategy component. The combination of higher returns and lower volatility creates a compounding advantage that dramatically improves long-term wealth accumulation.

Statistical improvements extend beyond simple return metrics. Rebalanced portfolios show lower correlation to Bitcoin during market crashes, providing genuine diversification benefits. When Bitcoin dropped 40% in a single week, rebalanced portfolios with altcoin exposure fell only 28% because the systematic buying of oversold assets created natural support levels.

“The magic of rebalancing isn’t just mathematical, it’s psychological. Knowing your system will automatically take profits removes the fear and greed that destroy most crypto traders.”

Pro Tip: Calibrate your rebalancing frequency by backtesting different intervals against your actual portfolio composition and historical volatility. What works for a Bitcoin-Ethereum portfolio differs dramatically from a portfolio with high-volatility DeFi tokens. Run simulations using three years of price data to identify the optimal balance between transaction costs and drift control for your specific holdings.

The cumulative effect of reduced drawdowns compounds powerfully over time. A portfolio that loses 50% requires a 100% gain to recover, while one that loses only 35% needs just 54% to break even. This asymmetry of losses makes downside protection through rebalancing one of the highest-value strategies in crypto investing.

Costs, pitfalls, and optimizing rebalancing frequency

High transaction fees and taxes reduce benefits for small portfolios or too frequent rebalancing; optimal quarterly or threshold methods recommend 10-15% drift. Understanding these friction costs is critical for implementing profitable rebalancing strategies rather than wealth-destroying ones.

Transaction fees in crypto include multiple layers. Exchange trading fees typically range from 0.1% to 0.5% per trade. Network gas fees for on-chain transactions can spike to $50-$200 during congestion. If you’re rebalancing a $10,000 portfolio weekly, these costs can easily consume 3-5% annually, completely erasing the rebalancing benefit.

Tax implications create even larger hidden costs for frequent rebalancing. Every rebalancing trade that sells an appreciated asset triggers a taxable event. In the US, short-term capital gains rates reach 37% for high earners, while long-term rates max at 20%. Monthly rebalancing can push all your gains into short-term treatment, effectively cutting your after-tax returns by 40-50%.

Frequent rebalancing destroys returns versus annual due to costs; manual rebalancing is less effective than automated. A portfolio rebalanced monthly might generate 15% gross returns but only 8% after fees and taxes, while quarterly rebalancing on the same portfolio yields 12% net returns.

Cost factors to consider before rebalancing:

- Trading fees multiply by the number of assets traded (rebalancing 10 coins costs more than 3)

- Spread costs from bid-ask differences can add 0.2-0.5% per trade

- Tax treatment varies dramatically by holding period and jurisdiction

- Opportunity cost of cash sitting in stablecoins during rebalancing execution

- Psychological cost of constant portfolio monitoring and decision fatigue

Behavioral discipline represents the most underestimated challenge in manual rebalancing. When Bitcoin pumps 30% in a week, selling a portion feels like leaving money on the table. When an altcoin crashes 50%, buying more feels like catching a falling knife. These emotional barriers cause most manual rebalancers to abandon their strategy at exactly the wrong moments.

Pro Tip: Calculate your breakeven rebalancing frequency by dividing your annual portfolio volatility by your round-trip transaction costs. If your portfolio experiences 60% annual volatility and costs 1% per round-trip rebalancing, you can profitably rebalance up to 60 times per year before costs exceed benefits. Most crypto portfolios optimize between 4-12 rebalances annually, suggesting quarterly to monthly frequencies work best.

Optimal rebalancing balances cost and risk control. Research consistently shows quarterly rebalancing or 10-15% drift thresholds capture most benefits while minimizing friction costs. Daily or weekly rebalancing only makes sense for very large portfolios where percentage costs are minimal or when using automated crypto trading systems that eliminate manual effort.

AI crypto trading benefits include optimized trade execution that waits for favorable market conditions rather than executing blindly on schedule. Smart algorithms can delay rebalancing trades by hours or days to capture better spreads, avoid high gas fees, or prevent front-running by market makers.

Automation minimizes human error and cost inefficiencies. Manual traders forget to rebalance, miscalculate position sizes, or execute trades in suboptimal order. Automated systems never forget, calculate perfectly, and optimize trade sequences to minimize total costs across the entire rebalancing operation.

Optimize your crypto portfolio with Darkbot AI automation

Managing portfolio rebalancing manually across multiple exchanges while optimizing for fees, taxes, and market timing creates overwhelming complexity. Darkbot eliminates this burden through AI-powered automation that executes sophisticated rebalancing strategies 24/7 without emotional interference or calculation errors.

Our platform connects to major exchanges via secure API integration, monitoring your portfolio allocations continuously and triggering rebalancing trades based on your chosen thresholds and strategies. Whether you prefer periodic, threshold-based, or dynamic AI-driven approaches, Darkbot adapts to your risk tolerance and investment goals while minimizing transaction costs through intelligent trade timing.

Cryptocurrency portfolio management becomes effortless when algorithms handle the mathematical complexity and execution discipline. You define your target allocations and rebalancing rules once, then let the system maintain optimal balance while you focus on research and strategy refinement. Real-time analytics show exactly how rebalancing improves your risk-adjusted returns compared to buy-and-hold alternatives.

Pro Tip: Start with conservative 15% drift thresholds and quarterly reviews when implementing automated rebalancing. Monitor your net returns after fees for three months, then gradually tighten thresholds to 10% if transaction costs remain manageable. This incremental approach lets you optimize frequency based on your actual portfolio characteristics rather than generic recommendations.

How often should I rebalance my crypto portfolio?

What rebalancing frequency works best for most crypto investors?

Quarterly rebalancing or 10-15% drift thresholds optimize the balance between capturing rebalancing benefits and controlling transaction costs for typical crypto portfolios. Monthly rebalancing generates excessive fees that erode returns, while annual rebalancing allows too much drift and concentration risk to accumulate. Research on crypto portfolios shows quarterly intervals capture 85-90% of potential rebalancing benefits while keeping costs under 1% annually. Threshold-based approaches work even better by responding to actual portfolio drift rather than arbitrary calendar dates, triggering rebalancing only when allocations meaningfully deviate from targets.

Can frequent rebalancing hurt my returns?

Yes, excessive rebalancing destroys returns through accumulated trading fees, unfavorable tax treatment, and opportunity costs. Each rebalancing cycle incurs exchange fees, network gas costs, and bid-ask spreads that compound quickly with frequent trading. More importantly, selling appreciated assets before the one-year holding period triggers short-term capital gains taxes at rates up to 37%, potentially cutting your after-tax returns in half compared to long-term treatment. Studies show monthly rebalancing typically underperforms quarterly approaches by 3-5% annually after accounting for all friction costs. Crypto rebalancing strategies must balance discipline with cost efficiency to add value.

How does automation improve rebalancing efficiency?

Automation enforces consistent discipline while optimizing trade execution timing, order routing, and cost minimization in ways manual traders cannot match. Automated systems monitor portfolios continuously across multiple exchanges, calculating optimal rebalancing trades instantly when thresholds trigger. They can split large orders to minimize market impact, wait for favorable spreads, avoid high gas fee periods, and execute trades during optimal liquidity windows. Perhaps most importantly, automation removes emotional interference that causes manual traders to abandon rebalancing strategies during market extremes. The advantages of automated crypto trading include eliminating calculation errors, execution delays, and psychological barriers that reduce manual rebalancing effectiveness by 20-40% compared to systematic automated approaches.

Can small crypto portfolios benefit from rebalancing despite fees?

Small portfolios under $10,000 face challenging economics with frequent rebalancing because fixed costs like gas fees consume disproportionate percentages of portfolio value. A $50 gas fee represents 0.5% of a $10,000 portfolio but 5% of a $1,000 portfolio, making frequent rebalancing uneconomical for smaller accounts. However, small portfolios can still benefit from rebalancing by using longer intervals (quarterly or semi-annual), higher drift thresholds (15-20%), and focusing rebalancing on exchange-based assets that avoid network gas fees. The cost of frequent rebalancing shows small portfolios should prioritize threshold-based approaches that minimize unnecessary trades while still controlling concentration risk during extreme market moves.

Recommended

- Portfolio rebalancing explained for crypto traders 2026

- Cryptocurrency Portfolio Balancing Guide for Automated Trading

- What is rebalancing in crypto? A 2026 guide for traders

- Automated Portfolio Management Explained: Smarter Crypto Investing

- Many-To-One Portfolio™ Framework (Merging Multiple Systems)

Start trading on Darkbot with ease

Come and explore our crypto trading platform by connecting your free account!