Machine Learning for Financial Forecasting: 2026 Guide

Machine Learning for Financial Forecasting: 2026 Guide

TL;DR:

- Machine learning enhances financial forecasting by capturing complex market patterns that traditional models miss.

- However, deploying ML in finance requires focus on explainability, continuous monitoring, and disciplined risk management strategies.

Machine learning for financial forecasting is defined as the application of adaptive, data-driven algorithms to analyze historical and real-time financial data and generate probabilistic predictions about future market behavior. Unlike traditional statistical models, ML systems update their parameters as new data arrives, making them structurally better suited to the nonlinear, non-stationary nature of financial markets. The global AI in finance market is projected to reach USD 1,045.60 billion, a figure that reflects how deeply predictive analytics has embedded itself across trading desks, risk teams, and portfolio management functions. Models like LSTM, FinGPT, and MSTFNet now represent the practical frontier of this field. This guide covers how these architectures work, where they outperform classical methods, and what it actually takes to deploy them in a production environment.

How does machine learning improve forecasting accuracy compared to traditional methods?

Traditional econometric models like ARIMA and GARCH operate on fixed assumptions: linearity, stationarity, and normally distributed errors. Financial markets violate all three assumptions regularly. Deep learning methods like LSTM, CNN, and Transformer architectures capture nonlinear temporal and cross-asset dynamics that classical models simply cannot represent. This gap becomes most visible during volatile periods, when ARIMA-based forecasts tend to lag or break down entirely.

The performance difference is measurable. The Multi-Scale Temporal Fusion Network (MSTFNet) reduces mean absolute error by 2% on S&P 500 and NASDAQ datasets compared to ARIMA by filtering noise in financial time series. That margin may sound modest, but in systematic trading, a consistent 2% reduction in forecast error compounds into material improvements in position sizing and risk-adjusted returns over time.

Hybrid models push accuracy further. Combining FinGPT sentiment analysis with historical price data reduces MSE to 46.06 and achieves an R² of 0.624 for AMD stock, outperforming both pure price-based models and traditional regression approaches. The R² value means the model explains roughly 62% of the variance in AMD’s price movement, a level of explanatory power that classical models rarely reach on individual equities.

Pro Tip: When benchmarking an ML model against ARIMA or GARCH, always test on out-of-sample data from a volatile period, such as a rate shock or earnings season. In-sample performance on calm data flatters every model equally.

| Model type | Strength | Limitation |

|---|---|---|

| ARIMA | Interpretable, fast to train | Assumes linearity and stationarity |

| GARCH | Models volatility clustering | Poor at directional price forecasting |

| LSTM | Captures long-term temporal dependencies | Computationally expensive, needs large datasets |

| MSTFNet | Filters multi-scale noise in time series | Newer architecture with less production history |

| Hybrid ALSTM-CNN-FinGPT | Best accuracy on NASDAQ and NYSE stocks | High complexity, harder to audit |

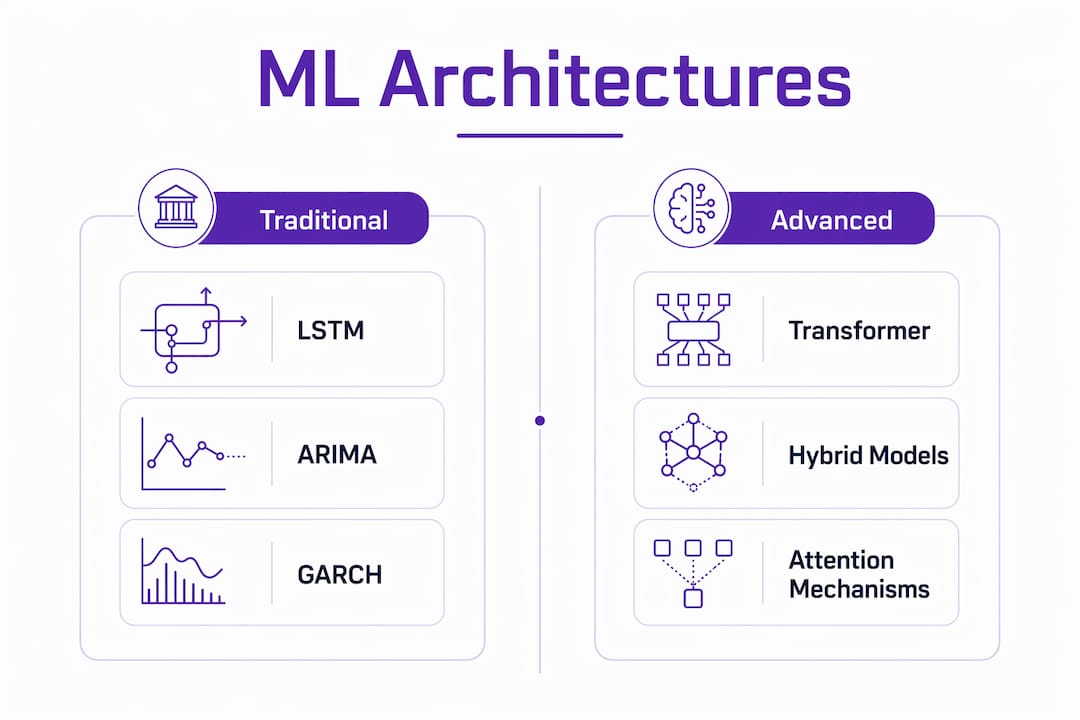

What are the leading ML architectures used in financial forecasting?

Long Short-Term Memory networks (LSTMs) remain the most widely deployed architecture for financial time series. An LSTM processes sequences of price and volume data while maintaining a memory cell that retains relevant information across hundreds of time steps. This makes it well suited for capturing patterns like earnings seasonality or multi-week momentum that shorter-window models miss entirely.

Transformer architectures and attention mechanisms have gained ground rapidly. Attention allows a model to weight the relevance of each past time step dynamically, rather than treating all history equally. This is particularly useful when a single macro event, such as a Federal Reserve rate decision, has outsized influence on subsequent price behavior. Transformers trained on financial data can learn to assign high attention weight to those inflection points automatically.

Convolutional Neural Networks (CNNs) contribute a different capability. CNNs excel at extracting local patterns from price charts and multi-asset correlation matrices. When stacked with LSTM layers, they handle both spatial feature extraction and temporal sequence modeling simultaneously. Hybrid attention-based models combining LSTM and CNN with FinGPT sentiment analysis deliver the best stock market forecasting accuracy across multiple NASDAQ and NYSE stocks by modeling both long-term dependencies and short-term market dynamics.

Key architectures finance analysts should understand:

- LSTM: Handles sequential price data with long memory windows; the standard baseline for time series forecasting in finance

- Transformer with attention: Dynamically weights historical events; effective for macro-driven assets and interest rate-sensitive instruments

- CNN: Extracts local price patterns and cross-asset correlations; most powerful when combined with recurrent layers

- MSTFNet: Filters noise across multiple time scales simultaneously; designed specifically for financial time series with mixed-frequency signals

- FinGPT: A Large Language Model fine-tuned on financial text; adds sentiment signals from earnings calls, news, and analyst reports to quantitative models

The direction of the field is clearly toward hybrid systems. No single architecture dominates across all asset classes or market regimes. The analysts who build the most durable forecasting systems treat architecture selection as an empirical question, not a default choice.

What challenges do finance professionals face integrating ML into forecasting workflows?

The biggest barrier to ML adoption in institutional finance is not accuracy. It is explainability. Black box syndrome inhibits adoption of highly accurate deep learning models because risk committees and regulators require auditable reasoning behind every forecast that influences a trading or lending decision. A model that achieves strong R² but cannot explain why it made a specific prediction creates legal and compliance exposure.

Professor Andrew Lo of MIT Sloan emphasizes that accountability and governance in AI models are critical to institutional adoption. Forecasting systems must be inherently transparent and verifiable, not just accurate. Large Language Models used as explanation layers address this directly. An LLM can translate a neural network’s output into plain-language reasoning that a portfolio manager or regulator can review and challenge.

Model drift is the second major operational challenge. A model trained on 2022 data will degrade when market structure shifts, as it did during the 2022 rate cycle or the 2024 crypto market recovery. Managing model drift requires continuous monitoring, scheduled retraining, and audit trails that satisfy compliance requirements. Most teams underestimate this ongoing maintenance burden when they first deploy.

Practical steps for managing integration challenges:

- Establish a data pipeline first. Building preprocessing pipelines for unstructured alternative data, such as earnings transcripts and news feeds, typically requires more resources than model development itself.

- Define explainability requirements before model selection. If your risk committee requires interpretable outputs, rule out pure black-box architectures from the start.

- Implement drift detection from day one. Set statistical thresholds that trigger retraining automatically when model performance degrades beyond an acceptable range.

- Document every model version. Regulatory audits require full traceability of model changes, training data, and performance metrics over time.

- Run shadow mode before live deployment. Let the model generate predictions in parallel with your existing process for at least one full market cycle before it influences real decisions.

Pro Tip: Treat your data pipeline as a product, not a one-time project. Assign a dedicated owner responsible for data quality, schema changes, and upstream feed reliability. Model performance degrades silently when data quality slips.

How can ML-enhanced forecasting support investment strategies and risk management?

Machine learning models improve forecasting speed and accuracy beyond rule-based systems, enabling proactive risk management and real-time decision-making in finance. The practical applications span the full investment process, from idea generation to execution and post-trade analysis.

Key use cases where ML forecasting delivers measurable value:

- Stock price prediction: LSTM and hybrid models generate directional forecasts for individual equities, informing entry and exit timing within systematic strategies

- Automated trading execution: ML signals feed directly into execution algorithms that adjust order sizing based on predicted volatility and liquidity conditions

- Portfolio optimization: Predictive models estimate forward-looking correlations between assets, improving diversification decisions beyond static historical covariance matrices

- Fraud detection: Classification models trained on transaction patterns flag anomalies in real time, reducing false positives compared to rule-based systems

- Crypto market applications: AI-powered platforms apply ML forecasting to digital asset markets, where price dynamics are faster and more sentiment-driven than traditional equity markets

The machine learning in fintech space has moved from experimentation to production deployment, particularly in crypto markets where 24/7 trading cycles and high volatility create conditions that favor automated, data-driven systems over manual analysis.

Risk management benefits from ML in a specific way. Traditional value-at-risk models assume normal return distributions and fixed correlations. ML models trained on tail events learn that correlations spike during stress periods, producing more conservative risk estimates precisely when they are most needed. This is not prediction of the future. It is pattern recognition applied to the conditions under which past losses occurred.

The AI trading strategy frameworks that perform best in production share one characteristic: they treat ML outputs as probabilistic inputs to a decision rule, not as certainties. The model generates a signal. The risk framework determines position size. The execution layer manages timing. Each layer operates independently, which limits the damage when any single component underperforms.

Proactive fraud detection also benefits from ML’s ability to process unstructured data at scale. ML in proactive fraud detection represents one of the clearest ROI cases in financial services, where the cost of a false negative far exceeds the cost of model development and maintenance.

Key Takeaways

Machine learning improves financial forecasting accuracy by capturing nonlinear market patterns that traditional models like ARIMA and GARCH cannot represent, but production deployment requires explainability, drift monitoring, and disciplined risk frameworks to deliver durable results.

| Point | Details |

|---|---|

| ML outperforms classical models | LSTM and MSTFNet reduce forecast error on S&P 500 and NASDAQ versus ARIMA baselines. |

| Hybrid architectures lead accuracy | Models combining LSTM, CNN, and FinGPT sentiment analysis achieve the best results on individual stocks. |

| Explainability blocks adoption | Black box models face regulatory resistance; LLM explanation layers improve trust and compliance. |

| Deployment is the hard part | Data pipelines, drift monitoring, and audit trails consume more resources than model development. |

| ML enables systematic risk control | Forecasting outputs work best as probabilistic inputs to rule-based decision frameworks, not as standalone signals. |

The gap between research accuracy and production reality

The research literature on ML forecasting is genuinely impressive. Hybrid models hitting R² values above 0.6 on individual stocks, MSTFNet cutting MAE on major indices, FinGPT adding sentiment signal that pure price models miss entirely. I find the empirical results credible. What I find less credible is the implicit assumption that these results transfer cleanly to a live trading environment.

The models in published research are trained and tested on clean, adjusted historical data. Production environments deal with feed outages, schema changes, corporate actions that distort price history, and regime shifts that make last year’s training data actively misleading. The gap between a model’s backtest performance and its live performance is not a technical failure. It is a structural feature of financial markets that no architecture eliminates.

My honest view is that the finance professionals who get the most from ML are not the ones chasing the highest R² on a benchmark dataset. They are the ones who build disciplined processes around model outputs: clear retraining schedules, hard position limits that do not flex based on model confidence, and explicit criteria for when a model gets taken offline. The machine learning in finance teams that last are the ones who treat their models as decision-support tools, not oracles.

The explainability challenge is real and underappreciated. A model that a risk committee cannot interrogate will not survive the first significant drawdown, regardless of its long-run accuracy. Building LLM explanation layers into your forecasting stack is not a nice-to-have. It is a prerequisite for institutional adoption.

— Grisha

Darkbot’s approach to ML-driven crypto trading

Finance professionals applying ML insights to crypto markets face the same core challenges: data quality, execution discipline, and risk control. Darkbot addresses these directly through an AI and machine learning foundation built for systematic trade execution across multiple digital asset exchanges.

Darkbot’s automated trading platform applies rule-driven logic and real-time analytics to crypto portfolio management, removing the manual execution layer that introduces inconsistency. The platform supports multiple simultaneous bots, strategy customization, and automated rebalancing, all governed by structured risk parameters rather than discretionary judgment. For analysts who want to apply ML forecasting principles to crypto without building infrastructure from scratch, Darkbot’s portfolio management tools provide a practical starting point.

FAQ

What is machine learning for financial forecasting?

Machine learning for financial forecasting is the use of adaptive algorithms, such as LSTM, Transformer networks, and hybrid deep learning models, to analyze financial data and generate probabilistic predictions about future price movements, volatility, and risk.

How does ML compare to ARIMA for stock forecasting?

ML models like MSTFNet reduce mean absolute error by 2% on S&P 500 and NASDAQ datasets compared to ARIMA by capturing nonlinear patterns and filtering noise that classical models cannot handle.

What is the biggest challenge in deploying ML models in finance?

The primary challenge is explainability. Deep learning models face regulatory resistance because risk committees require auditable reasoning behind forecasts, and black box outputs create compliance exposure in institutional environments.

What role does FinGPT play in financial forecasting?

FinGPT is a Large Language Model fine-tuned on financial text. When integrated with price-based models, it adds sentiment signals from news and earnings data, reducing MSE to 46.06 and achieving R² of 0.624 for AMD stock in hybrid model tests.

How does ML support risk management in finance?

ML models trained on historical stress periods learn that asset correlations spike during market dislocations, producing more conservative risk estimates when conditions resemble past tail events. This supports proactive risk management beyond what static value-at-risk models provide.

Recommended

Start trading on Darkbot with ease

Come and explore our crypto trading platform by connecting your free account!