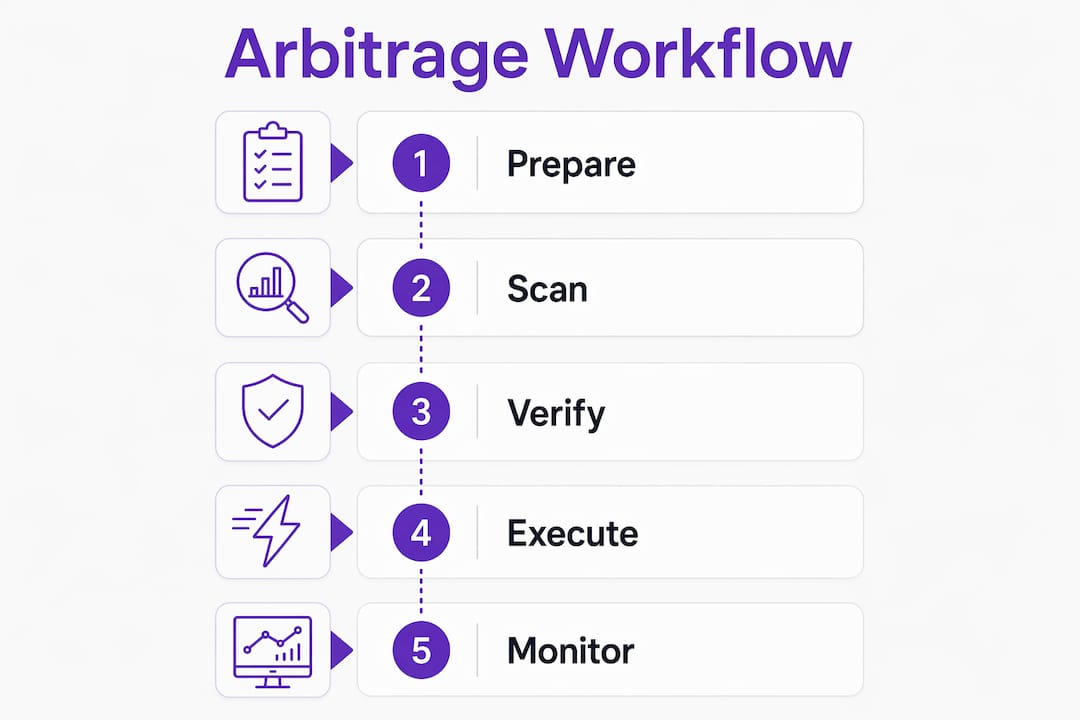

Step by Step Arbitrage Workflow for Crypto Traders

Step by Step Arbitrage Workflow for Crypto Traders

TL;DR:

- Crypto arbitrage requires pre-funded accounts, low-latency systems, and automated execution to capture rapid price differences. Manual trading cannot compete with bots that operate within milliseconds, making full automation essential for success. Effective risk management, system testing, and monitoring are critical to avoid costly operational failures.

A step-by-step arbitrage workflow is a structured execution process that captures price differences for the same asset across two or more exchanges, converting those differences into realized profit after fees. In crypto markets, this process is known formally as statistical arbitrage or cross-exchange arbitrage, and it demands speed, capital preparation, and disciplined risk controls. Opportunity windows on major pairs last fewer than 4 seconds, which means manual execution is rarely viable. The minimum profitable spread for CEX-to-CEX trades sits at 0.15% to 0.25%, rising to 0.3%–0.5% for DEX-to-CEX routes. Any trader who skips the preparation phase or underestimates fee drag will lose capital before a single profitable trade closes.

What prerequisites are required to begin crypto arbitrage trading?

Preparation is the phase most traders underestimate, and it is where the majority of avoidable losses originate. Before executing a single trade, you need funded accounts on at least two exchanges, a clear picture of your fee structure, and a tested technical setup.

Capital allocation and exchange accounts

Pre-funding capital on both exchanges is the foundational requirement for simultaneous execution. A common starting structure places $5,000 on each exchange, giving you $10,000 in total deployed capital. Without pre-funded wallets on both sides, you will face transfer delays that erase the spread before your trade settles. Every exchange also requires KYC verification, and withdrawal limits vary significantly, so confirm those limits before committing capital.

Fee structure and technical tools

Trading fees on centralized exchanges typically run 0.02%–0.1% per side. That means a round trip costs up to 0.2%, which consumes the entire minimum spread on a marginal opportunity. You need to know your exact fee tier before calculating whether any spread is worth pursuing.

The technical setup for a functional arbitrage process requires several components working together:

- Exchange API keys configured with trade permissions on each platform

- Arbitrage scanner or live data feed to detect price discrepancies in real time

- Automated trading bot capable of submitting simultaneous orders

- Order book monitoring tool to assess depth and exit liquidity

- Latency monitoring to confirm your system operates below the 5-millisecond threshold required for competitive execution

Pro Tip: Run a small test trade of $50–$100 on each exchange before committing full capital. This confirms API connectivity, fee deductions, and order routing before a misconfiguration costs you real money.

Liquidity management is not a secondary concern. Treat inventory balancing across exchanges as active portfolio management, not an afterthought. Rebalance periodically to keep capital available on both sides.

How do you identify and evaluate profitable arbitrage opportunities?

Identifying a valid opportunity requires more than spotting a price difference. You need to confirm that the spread survives fees, that sufficient liquidity exists on both sides, and that the opportunity has not already closed by the time your order reaches the market.

Scanning and spread calculation

Arbitrage scanners pull live order book data from multiple exchanges and flag pairs where the bid on one exchange exceeds the ask on another. The raw spread is not your profit. Your net profit equals the gross spread minus taker fees on both sides, minus any gas costs for on-chain routes. A 0.4% spread on a DEX-to-CEX route with 0.1% fees per side leaves only 0.2% net, which may not justify the execution risk.

Key criteria for evaluating an opportunity:

- Net spread clears the fee threshold (0.15%–0.25% for CEX-to-CEX; 0.3%–0.5% for DEX-to-CEX)

- Order book depth supports your full position size without moving the market against you

- Exit liquidity exists on the sell side at the expected price

- The spread is a plateau, not a spike — a spike often collapses before your order fills

- Opportunity age is under 2 seconds — stale alerts from slow feeds are a direct path to losses

Cross-exchange vs. triangular arbitrage

Cross-exchange arbitrage buys an asset on one exchange and sells it on another. Triangular arbitrage exploits price inefficiencies between three trading pairs on a single exchange, converting Asset A to B, B to C, and C back to A. Triangular routes eliminate transfer risk but require more complex order sequencing and tighter fee calculations. Both methods follow the same core arbitrage trading steps: identify, calculate, execute, and exit.

Pro Tip: Never act on an alert older than a few seconds. Always verify the spread in real time against the live order book before submitting an order.

How to execute a crypto arbitrage trade from start to finish

Execution is where preparation either pays off or fails. The goal is simultaneous order placement on both exchanges, with pre-funded wallets eliminating any dependency on fund transfers during the trade.

The execution sequence

- Confirm the live spread against the current order book on both exchanges, not the scanner alert.

- Verify order book depth on both the buy and sell sides to confirm your position size fits without slippage.

- Submit simultaneous orders via API: a market or aggressive limit buy on the lower-priced exchange and a sell on the higher-priced exchange.

- Monitor fill status on both legs within the first 500 milliseconds. A partial fill on one leg creates an open, unhedged position.

- Handle partial fills immediately: either complete the fill with a follow-up order or close the open leg at market to eliminate directional risk.

- Confirm net settlement after both legs close, accounting for actual fees charged.

- Log the trade with spread, fees, slippage, and net result for performance review.

Professional execution systems operate with latency under 5 milliseconds. That standard reflects the reality that most opportunities close within 4 seconds. Any system slower than that competes at a structural disadvantage.

Execution risks include partial fills, liquidity depletion mid-order, and API failures. These are not edge cases. They occur regularly, and managing them requires continuous monitoring during every active trade, not just at entry.

Pro Tip: Set automated alerts for API latency spikes and order book jumps. A 50-millisecond latency increase during a trade can mean the difference between a filled order and a missed execution.

Exit depth monitoring matters as much as entry. If the sell-side order book thins out after you enter the buy leg, your exit price degrades and your net spread shrinks or turns negative. Build exit monitoring into your bot logic from the start.

What are the common challenges in a crypto arbitrage workflow?

Arbitrage trading carries real execution risk. Recognizing the failure points before they occur is the difference between a recoverable error and a significant capital loss.

Fund transfer delays and capital imbalance

Waiting for fund transfers is one of the most common failure points in arbitrage. If your capital is concentrated on one exchange after a series of trades, you cannot execute on the other side. Professional traders pre-fund both exchanges and rebalance periodically during low-activity periods, not during active trading windows.

Key challenges and their mitigations:

- Network congestion on on-chain routes: Use gas price monitoring and set maximum gas limits to avoid overpaying during congestion spikes.

- Partial fills and liquidity depletion: Size positions relative to order book depth, not your total capital.

- Trading fatigue in manual workflows: Automate repetitive monitoring tasks. Human attention degrades over multi-hour sessions.

- MEV bot frontrunning on DEX routes: Use private RPCs like Flashbots Protect to hide transactions until block inclusion, reducing sandwich attack exposure.

Flashbots Protect routes your transaction through a private mempool, preventing MEV bots from seeing and frontrunning your order before it settles on-chain.

Pro Tip: Run trial executions with minimal capital, around $50–$100, to identify system weaknesses before scaling. Small tests surface misconfiguration, fee errors, and latency issues at low cost.

Trial runs with small capital are a recognized best practice for testing bot and exchange response before committing larger positions. This applies equally to new traders and experienced traders deploying a new bot configuration.

How does automation improve the arbitrage workflow?

Profitable arbitrage in 2026 is almost entirely automated. Manual execution on mainstream pairs is not competitive. Bots scan thousands of pairs simultaneously, submit orders in milliseconds, and apply rule-based risk controls without hesitation or fatigue.

What automation handles in a modern arbitrage system

- Continuous scanning across multiple exchanges and pairs, 24 hours a day

- Real-time spread calculation including fees, gas costs, and slippage estimates

- Simultaneous order submission via API with sub-millisecond response times

- Partial fill detection and automated hedging of open legs

- Risk limit enforcement: position size caps, daily loss limits, and drawdown stops

- Portfolio rebalancing to maintain capital availability across exchanges

Integrating automated trading systems with portfolio management creates a closed-loop workflow. Capital is allocated, deployed, and rebalanced without manual intervention at each step.

Automation does carry its own risks. API keys require strict security controls, including IP whitelisting and read/trade-only permissions with no withdrawal access. Bot configurations need regular audits because market conditions change and a rule set that worked in one volatility regime may perform poorly in another.

Pro Tip: Audit your bot configuration at least monthly. Review fill rates, slippage averages, and fee costs against your original assumptions. Markets shift, and static configurations drift out of alignment.

The advantages of automated crypto trading extend beyond speed. Automation removes emotional decision-making from the execution loop, which is one of the most consistent sources of loss in discretionary trading.

Key takeaways

A complete arbitrage execution plan requires pre-funded capital, sub-5-millisecond system latency, and automated order management to capture spreads that close in under 4 seconds.

| Point | Details |

|---|---|

| Pre-fund both exchanges | Place capital on each exchange before trading to enable simultaneous execution without transfer delays. |

| Know your fee threshold | CEX-to-CEX spreads need at least 0.15%–0.25% net to be profitable after fees. |

| Automate execution | Manual trading cannot compete on mainstream pairs; bots scan and execute in milliseconds. |

| Monitor exit depth | Order book depth on the sell side matters as much as entry conditions for net profit. |

| Use private RPCs on DEX routes | Flashbots Protect reduces frontrunning risk by hiding transactions until block inclusion. |

What I’ve learned from watching traders execute arbitrage workflows

Most traders who fail at arbitrage do not fail because of a bad strategy. They fail because they underestimate the operational complexity. The workflow looks simple on paper: buy low, sell high, pocket the spread. The reality involves API latency, partial fills, fee drag, capital imbalance, and market microstructure that shifts faster than most traders can process manually.

The traders I have seen execute this well share one trait: they treat the workflow as an engineering problem, not a trading opportunity. They spend more time on system design, testing, and configuration than on market analysis. They run small tests obsessively before scaling. They build monitoring into every layer of the system, not just the entry point.

The shift toward full automation is not optional for anyone trading liquid pairs. Automation dominates profitable arbitrage precisely because the human execution loop is too slow and too inconsistent. The traders who resist automation tend to find themselves chasing opportunities that closed 3 seconds before their order arrived.

Discipline in risk management matters more than finding the perfect spread. A trader who caps daily losses, sizes positions correctly, and rebalances capital systematically will outperform a trader who chases high-spread opportunities without controls. The workflow is the edge, not the individual trade.

— Grisha

Darkbot and automated arbitrage execution

Darkbot is built for traders who want systematic arbitrage execution without rebuilding infrastructure from scratch. The platform connects to multiple exchanges via API, submits simultaneous orders across trading pairs, and applies rule-based risk controls at every step of the automated arbitrage workflow. Portfolio management tools handle capital rebalancing across exchanges, keeping funds available on both sides without manual intervention. Darkbot’s AI-driven logic evaluates spreads, monitors order book depth, and enforces position limits continuously. Traders can configure multiple bots across different pairs and strategies, with real-time analytics tracking performance at the trade level. For traders ready to move from manual execution to a structured, automated system, Darkbot provides the infrastructure to do it.

FAQ

What is a step by step arbitrage workflow?

A step-by-step arbitrage workflow is a structured process for capturing price differences across exchanges, covering capital setup, opportunity identification, simultaneous order execution, and post-trade monitoring. Each step must complete within defined time and fee thresholds to produce a net profit.

How much capital do I need to start crypto arbitrage?

A common starting structure pre-funds $5,000 on each of two exchanges, totaling $10,000 in deployed capital. Smaller amounts are possible for testing, but thin position sizes make fee drag proportionally larger.

Why is automation necessary for crypto arbitrage?

Profitable arbitrage on mainstream pairs is almost entirely automated in 2026 because opportunity windows close in under 4 seconds and professional systems require latency under 5 milliseconds. Manual execution cannot meet those standards consistently.

What is the minimum profitable spread for CEX-to-CEX arbitrage?

The minimum profitable spread for CEX-to-CEX arbitrage is 0.15%–0.25%, accounting for taker fees of 0.02%–0.1% per side. DEX-to-CEX routes require 0.3%–0.5% to cover higher gas and fee costs.

How do I protect against MEV bot attacks in DEX arbitrage?

Use private RPCs such as Flashbots Protect to route transactions through a private mempool. This prevents MEV bots from seeing your transaction before block inclusion, reducing sandwich attack and frontrunning exposure.

Recommended

Start trading on Darkbot with ease

Come and explore our crypto trading platform by connecting your free account!