Optimize automated crypto trading: 152%+ returns safely

Optimize automated crypto trading: 152%+ returns safely

TL;DR:

- Hybrid RL/ML frameworks can significantly improve crypto trading returns and reduce drawdowns.

- Smarter data sampling methods like dollar bars and CUSUM filtering enhance signal quality over traditional time bars.

- Effective risk management and regular strategy validation are crucial to sustain profitability in automated trading.

Most automated crypto trading systems bleed performance quietly. Outdated data sampling, rigid model configurations, and zero adaptive risk logic turn promising bots into expensive disappointments. The good news? Research now shows that hybrid RL/ML frameworks like GBRT prediction paired with Deep RL can achieve 152% or more in excess returns while cutting maximum drawdown to 19.3%. This guide walks you through every layer of a high-performance automated trading system: the right tools, smarter data pipelines, proven ML and reinforcement learning models, and the risk controls that keep gains from evaporating.

Key Takeaways

| Point | Details |

|---|---|

| Advanced data sampling | Switching to CUSUM, range, or volume bars plus smarter labeling boosts trade signal reliability and results. |

| ML and RL models | Hybrid and adaptive machine learning models can deliver significantly higher returns and better risk-adjusted outcomes in volatile crypto markets. |

| Thorough risk management | Dynamic reward structures and exhaustive backtesting are essential to protecting gains and minimizing losses in automated trading. |

| Continuous adaptation | Success with bots requires ongoing validation and flexibility—not just one-time model tuning. |

What you need to optimize your trading bot

Optimizing your trading bot is not just about swapping in a new algorithm. It requires rethinking the entire stack, from how you collect and sample market data to how your model learns and adapts under pressure. Before you touch a single line of config, make sure you have the right foundation.

Here is what your setup needs to include:

- Exchange account with API access: Binance, Coinbase Advanced, Kraken, or similar. API keys must have trading permissions enabled.

- Minimum capital buffer: At least $500 to $1,000 for meaningful backtesting and live performance comparison.

- Compute resources: A cloud instance or local machine with at least 8GB RAM for running ML training jobs.

- Software platforms: Python-based environments (scikit-learn, stable-baselines3, FinRL) or SaaS tools with built-in machine learning tools for strategy deployment.

- Data feed: Tick-level or minute-level OHLCV data from your target exchange.

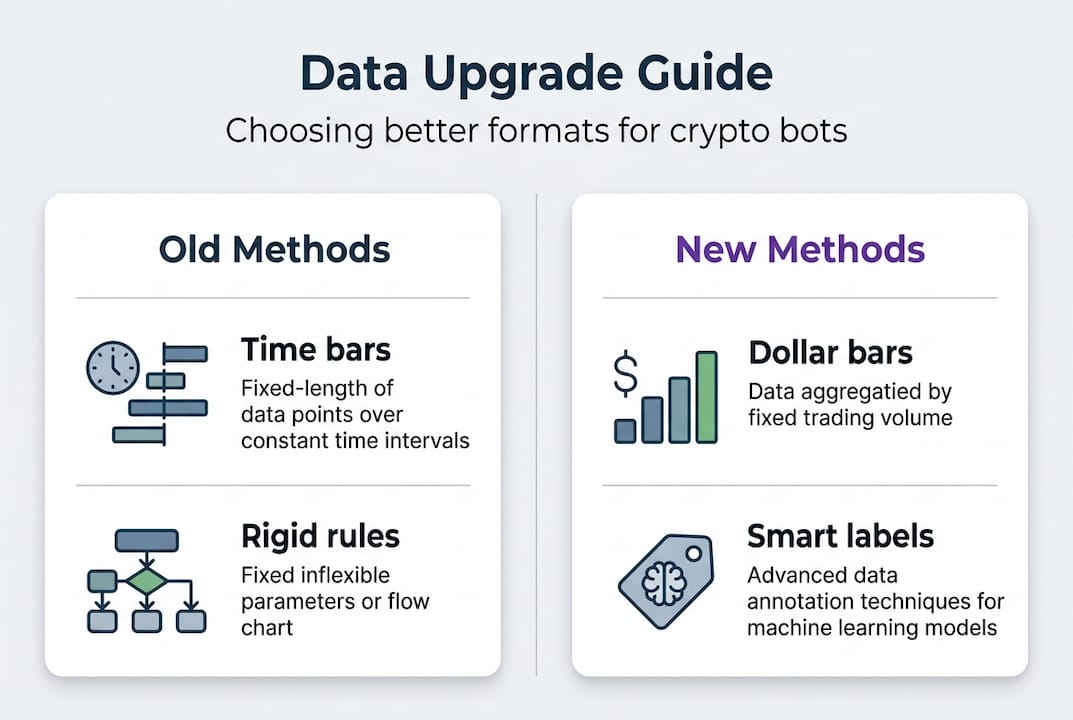

One of the most overlooked upgrades is switching your data format. Information-driven data sampling consistently outperforms traditional time bars in BTC and ETH trading by capturing market activity based on actual events rather than fixed clock intervals.

| Data type | Basis | Signal quality | Best for |

|---|---|---|---|

| Time bars | Fixed intervals | Moderate | Simple strategies |

| Volume bars | Fixed volume | High | Liquid pairs |

| Dollar bars | Fixed dollar value | Very high | Cross-asset comparison |

| CUSUM bars | Statistical filter | Highest | Trend detection |

Pro Tip: Before rebuilding your entire pipeline, run a quick backtest comparing your current time-bar data against dollar bars on the same strategy. The performance gap often justifies the switch immediately.

If you are new to setting up this kind of AI automation workflow, start with dollar bars and a single ML model before layering in reinforcement learning.

Configuring advanced data sampling and labeling

Time-based bars are the default for most trading platforms, but they create a hidden problem. They treat a quiet Sunday afternoon the same as a volatile post-Fed-announcement hour. That means your model trains on noise as much as signal, diluting its ability to identify real opportunities.

Here is how to configure smarter data sampling step by step:

- Choose your bar type. Start with dollar bars for BTC/USDT. Set the threshold at roughly 1 million USD per bar to balance granularity and computation.

- Apply CUSUM filtering. Use a cumulative sum filter on price changes to trigger a new bar only when a statistically meaningful shift occurs. This removes microstructure noise.

- Set volume bar thresholds. For altcoins with lower liquidity, volume bars (e.g., 500 BTC per bar) often outperform dollar bars by reflecting actual market participation.

- Label your data with Triple Barrier. Define an upper profit target, a lower stop-loss level, and a time limit for each trade. The first barrier hit determines the label.

- Validate label distribution. Aim for a balanced split between long, short, and neutral labels. Heavy imbalance signals a flawed threshold setup.

Triple barrier research confirms that pairing information-driven sampling with Triple Barrier labeling enables strategies that consistently outperform time bars on BTC and ETH.

| Sampling method | Signal detail | Ideal use case |

|---|---|---|

| Time bars | Low | Baseline testing |

| Volume bars | Medium | Mid-cap altcoins |

| Dollar bars | High | BTC, ETH majors |

| CUSUM bars | Very high | Trend-following systems |

Pro Tip: Run your backtest twice on the same date range, once with time bars and once with dollar bars, and compare the Sharpe ratio. Most traders see a 15 to 30% improvement in risk-adjusted returns just from this switch.

Once your data pipeline is clean, you are ready to build smarter crypto strategies on top of reliable signals rather than calendar-driven noise. A well-labeled dataset is the foundation that every trading strategies breakdown depends on.

Applying machine learning frameworks and deep reinforcement learning

With a clean data pipeline in place, the next step is choosing the right model architecture. Not all ML and RL approaches perform equally across different coins and market conditions.

Here is a breakdown of the four most relevant frameworks:

- GBRT (Gradient Boosted Regression Trees): Excellent for feature-rich, tabular trading data. Works well as a signal generator feeding into an RL agent.

- Rainbow DQN: Combines multiple DQN improvements for discrete action spaces. Best suited for trending markets like ETH/USDT.

- SAC (Soft Actor-Critic): Handles continuous action spaces and balances exploration vs. exploitation. Strong in sideways or mixed-regime markets.

- DDQN (Dueling Double DQN): Reduces overestimation bias. Performs well on assets with lower liquidity like XRP.

The performance data here is hard to ignore. Hybrid RL/ML research shows that combining GBRT with Rainbow DQN or SAC achieved 287% returns on ETH/USDT, a Sharpe ratio up to 2.81, and reduced maximum drawdown by more than half. Separately, Duelling/DDQN delivered 204% returns versus 124% for buy-and-hold on XRP.

“Even the best-performing models carry risk. Overfitting to historical data and backtest bias are among the most common failure modes in crypto RL systems. Always validate on out-of-sample data before live deployment.”

To integrate two frameworks side by side, train GBRT on your labeled dataset to generate a probability score for each bar. Feed that score as a feature into your RL agent alongside raw price data. Run both a GBRT-only strategy and the hybrid in parallel backtests. Compare Sharpe, max drawdown, and win rate before committing capital.

Understanding AI’s role in volatile markets is critical here. These models do not eliminate risk. They shift the probability in your favor when configured correctly. For a deeper look at optimizing ML crypto trading, the architecture choices matter as much as the data.

Risk management, testing, and common pitfalls

Even a well-tuned model fails without disciplined risk controls. This is where most traders lose gains they worked hard to build.

Follow these steps to embed robust risk management:

- Set a hard maximum drawdown limit. Cap drawdown at 20 to 25% of your portfolio. If your bot hits this threshold, it pauses and alerts you.

- Define slippage tolerance. Set a maximum acceptable slippage per trade (typically 0.1 to 0.3% for liquid pairs). Reject trades that exceed it.

- Apply position sizing rules. Use Kelly Criterion or fixed fractional sizing. Never risk more than 2% of capital per trade.

- Run walk-forward testing. Train on a fixed window, test on the next period, then roll forward. Repeat across at least 12 months of data.

- Validate with out-of-sample data. Reserve at least 20% of your dataset for final validation. Never optimize on this portion.

Common pitfalls to avoid:

- Overfitting: A model that memorizes historical patterns fails in live markets. Watch for suspiciously high backtest Sharpe ratios above 3.5.

- Regime blindness: Markets shift from trending to ranging without warning. Static models decay fast.

- Hidden fees: Exchange fees, funding rates, and withdrawal costs erode retail advantages faster than most traders expect.

“Crypto’s fat tails and sudden regime changes mean that backtest results almost always overstate live performance. Build your risk framework assuming your model is partially wrong at all times.”

Dynamic rewards reduced max drawdown from 42.7% to 19.3% in diversified quant strategies, with a beta of just 0.038, showing how disciplined risk architecture separates consistent performers from one-hit wonders.

For practical frameworks, explore smart crypto risk automation, detailed bot risk strategies, and guidelines for safer crypto trading that apply directly to live bot deployments.

Why the best automated trading isn’t just about algorithms

Here is the uncomfortable truth most bot vendors will not tell you: algorithms are the easy part. The hard part is staying honest with yourself about what is actually working and why.

Markets do not reward clever code. They reward adaptive processes. A model that crushed it in Q1 2025 may be quietly bleeding in Q3 2026 because the regime shifted and nobody noticed. Crypto’s high volatility and fat tails demand adaptive RL over static models, and overfitting with backtest bias remain the most common failure modes across the industry.

The traders who compound consistently are not the ones with the most sophisticated models. They are the ones who schedule monthly re-validation of every assumption: data quality, label logic, risk thresholds, and fee structures. They treat their bot like a living system, not a finished product.

Pro Tip: Set a calendar reminder every 30 days to re-run your walk-forward test on fresh data. If your Sharpe drops more than 20% from your baseline, treat it as a red flag and investigate before adding capital.

As Coin Bureau notes, bots can amplify a strategy, but fees, slippage, and volatility erode retail advantages in ways that are invisible until they are not. The discipline to question your own strategy execution realities is what separates profitable automation from expensive experimentation.

Automate smarter: Next steps with Darkbot

Ready to implement these upgrades? Here is how to accelerate your crypto trading automation journey.

Darkbot’s AI trading bot solutions are built for exactly this kind of layered optimization. Whether you are configuring your first bot or upgrading an existing strategy with dynamic risk controls and ML-driven signals, the platform handles data integration, strategy customization, and real-time analytics in one place. The portfolio optimization features let you manage automated rebalancing and risk exposure across multiple exchanges simultaneously. From free-tier exploration to premium multi-bot deployments, Darkbot gives you the infrastructure to act on everything covered in this guide without building it from scratch.

Frequently asked questions

What is the Triple Barrier method, and how does it improve signal accuracy?

The Triple Barrier method assigns trade labels by setting a profit target, a stop-loss level, and a time expiry, so whichever limit is hit first determines the label. This produces cleaner, more actionable signals than simple up/down directional labeling, and Triple Barrier labeling has been shown to outperform traditional time bars on BTC and ETH.

How do deep RL agents like Rainbow DQN beat buy-and-hold in crypto?

Deep RL agents continuously adapt their actions based on market feedback rather than following a fixed rule set, allowing them to capture trends and sidestep drawdowns more effectively. Research shows Rainbow DQN achieved 287% on ETH/USDT, while RL on XRP delivered 204% versus 124% for buy-and-hold.

What are the biggest risks with automated trading bots?

The main risks are overfitting to historical data, market regime changes, drawdowns, and the cumulative drag of fees, slippage, and volatility that erode retail advantages over time. Robust walk-forward testing and hard drawdown limits are your best defenses.

Do I need coding skills to apply these automation optimizations?

Not necessarily. Modern platforms like Darkbot support no-code and low-code configuration for advanced sampling, ML strategy selection, and risk controls, though custom Python frameworks offer deeper tuning flexibility for experienced users.

Recommended

Start trading on Darkbot with ease

Come and explore our crypto trading platform by connecting your free account!